Why AI Value Creation and Value Capture Are Diverging

AI adoption (at some level) is now nearly universal. Durable AI value creation is not.

That gap is the single most important signal emerging from the 2025 data. Two independent reports, Battery Ventures’ “State of AI Report” (December 2025) and McKinsey / QuantumBlack’s “State of AI in 2025”, tell the same story from different vantage points.

Capital markets have effectively created two asset classes. AI-Native trading at 15x+ revenue, and Legacy SaaS trading at ~4x revenue.

I previously outlined the specific playbook for re-rating these pre-AI assets, but the latest 2025 data confirms exactly why that strategy is urgent. The market isn't just rewarding growth; it is pricing a fundamental architectural shift.

For the executive or investor, the mandate is no longer about "adopting" AI. It is about crossing that chasm. Public markets are no longer debating whether AI matters; they are pricing who has successfully re-architected to monetize it.

What the Data Shows

According to the Battery report, since the launch of ChatGPT, AI-exposed companies have added roughly $18 trillion in market capitalization, representing about 75% of all S&P 500 gains over that period. The market has paid for the revolution in advance.

In contrast, the enterprise data shows a distinct lag. McKinsey’s report highlights a "pilot purgatory". Nearly 90% of organizations use AI, but fewer than half report any measurable EBIT impact.

The implication is clear. The market has priced in a transformation that most organizations have not yet operationally delivered.

Structural Inflection Points

The data points to three structural shifts that will determine which companies close the valuation gap in 2026.

First: Workflow redesign is the only metric that matters. Adoption metrics are vanity metrics. As McKinsey notes, the strongest predictor of value isn't model access. It is the extent of workflow redesign. Simply plugging a model into a legacy process yields incremental efficiency. Rebuilding the process around the model yields enterprise value.

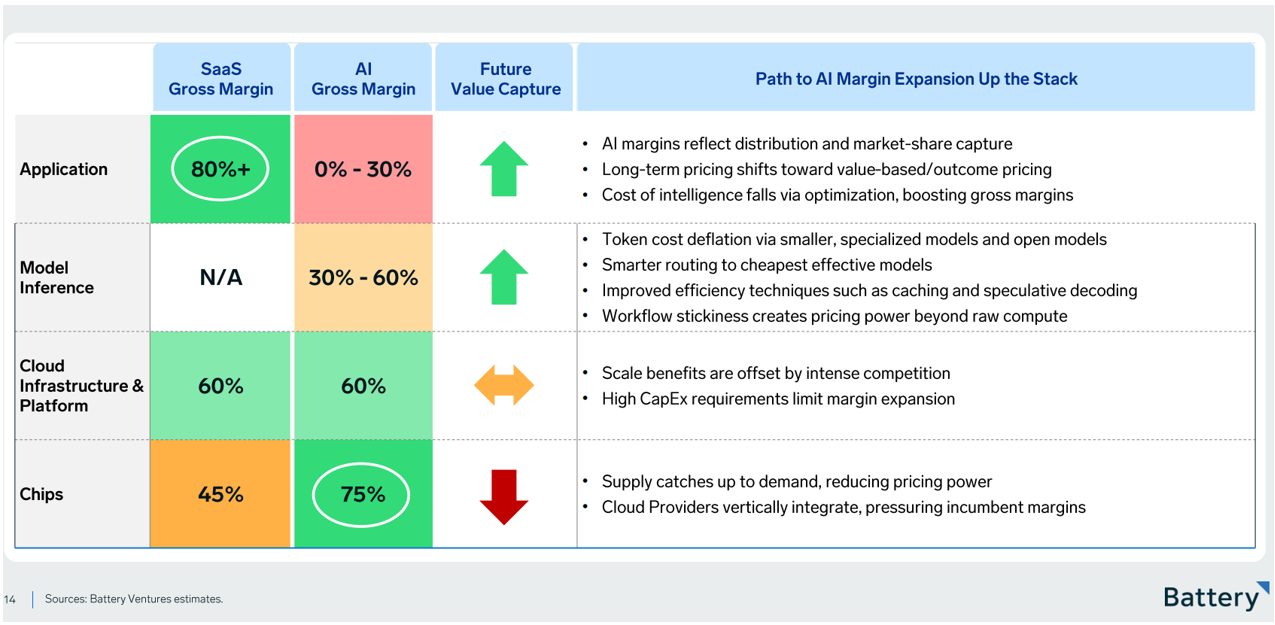

Second: The "Margin Flip." We are currently in a phase where infrastructure captures the profit. However, as Battery Ventures outlines, we are approaching a tipping point. As inference costs collapse ("token deflation") and models commoditize, value capture will move up the stack to the application layer. But only for applications that own the end-to-end workflow.

Source: Battery Ventures State of AI Report 2025

Third: The Moat is "System Coherence," not Intelligence. Durable advantage no longer comes from having the best model. It comes from having the best feedback loop. The winners are building systems where every interaction sharpens the underlying data asset, creating a compounding advantage that generic models cannot replicate.

The Three Outcomes

From my perspective, companies will land in one of three buckets based on how they translate these inflection points into M&A and strategy.

Outcome 1: AI as Surface Area (The "Copilot" Trap)

In this outcome, AI expands the surface area of existing products without changing their underlying structure.

This is the default path for most incumbents. Companies layer "Copilots" and assistants onto legacy systems of record. While productivity gains are real, they are localized. Humans still own the workflow, AI merely assists.

M&A and partnership deals here are feature-driven or talent-driven ("acqui-hires"). Integration is often light to avoid disrupting the core business.

Salesforce’s partnership with OpenAI is a great example. While Salesforce is pushing Agentforce aggressively, for many customers, the reality is still "Surface Area AI." The core CRM data model remains largely intact, and AI serves as a query interface rather than a fundamental restructuring of how sales get done. This preserves relevance, but it does not trigger a valuation re-rating.

Outcome 2: AI as a System (The Winners)

Here, AI is not added to workflows; workflows are rebuilt around AI.

M&A is used to buy a structural advantage faster than it can be built. Companies in this bucket don't just buy "features”. They buy Reasoning Engines and Decision Intelligence that span across departments.

M&A deals target "System of Action" capabilities. Post-merger integration (PMI) is rigorous, focusing on unifying data layers to enable agentic behavior. Some recent examples include:

ServiceNow + Moveworks: This wasn't just a chatbot acquisition. It was the acquisition of a "Reasoning Engine" capable of autonomous resolution across IT, HR, and CS. It accelerated ServiceNow's shift from a System of Record to a System of Action, replacing human ticketing with machine execution.

UiPath + Peak: By acquiring Peak, UiPath moved beyond "Task Automation" (RPA) into "Decision Intelligence." This allows them to orchestrate complex, non-linear workflows, moving their value proposition from "saving hours" to "improving business outcomes."

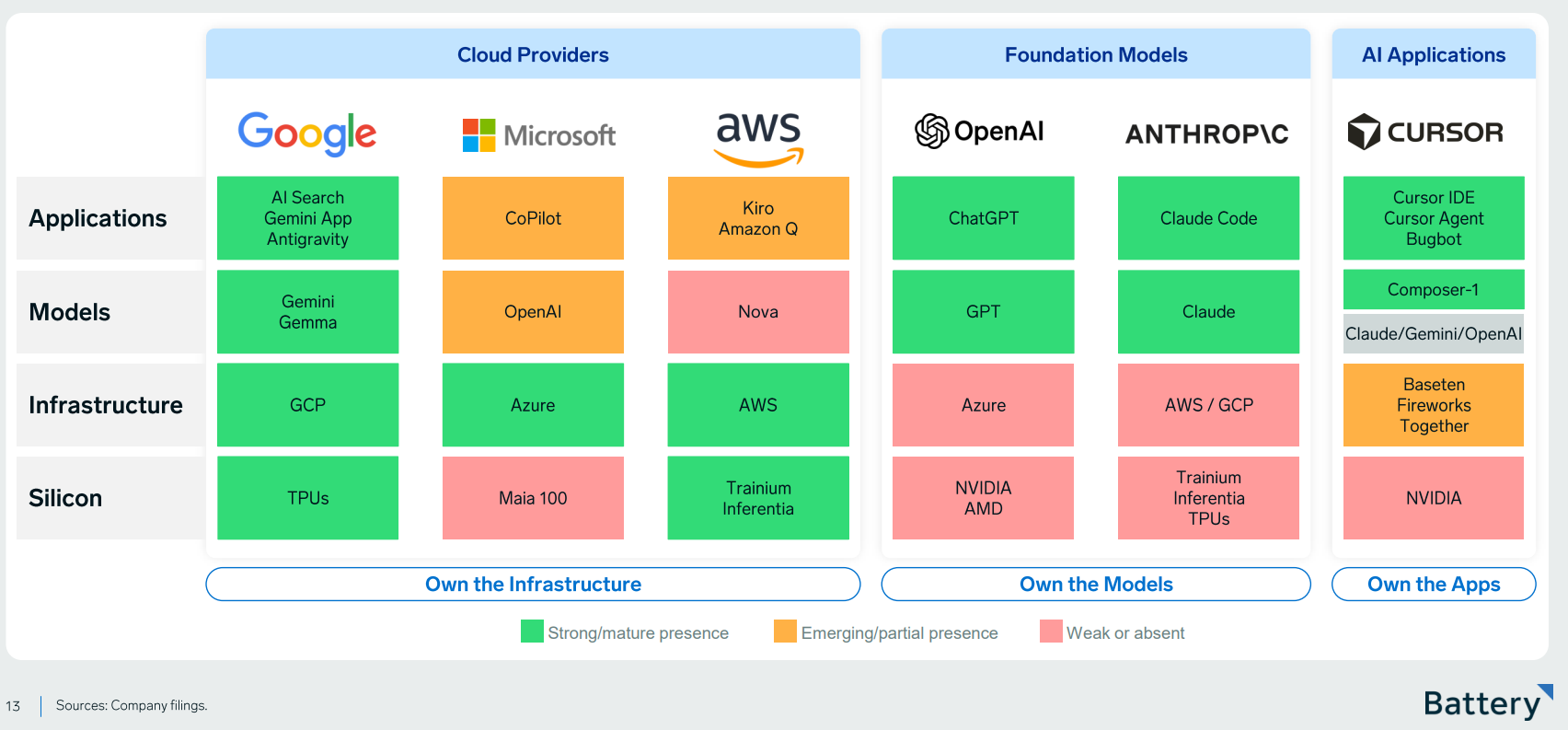

Outcome 3: Infrastructure (The Vertical Defense)

This outcome applies to hyperscalers. M&A here is defensive, driven by the need to secure supply chains and defend against commoditization.

These players would continue revenue growth driven by training and inference demand. There is a need for massive capital investment to stay competitive, and high capital intensity would limit free cash flow expansion. Vertical integration across silicon, infrastructure, models, and platforms will continue. There would be increasing competition and customer sophistication around cost. Margins would normalize over time as supply catches up and differentiation compresses.

Source: Battery Ventures State of AI Report 2025

Microsoft & Amazon are both great examples. Both are aggressively moving up-stack (via OpenAI and Anthropic) because they know that raw compute margins will eventually compress. They are using their balance sheets to vertically integrate before the "Margin Flip" occurs.

Where the Reports Fall Short

Both reports are excellent at diagnosing the what, but they understate the difficulty of the how. Specifically, they don’t cover integration and organizational readiness elements deeply enough.

The Integration Tax: Battery and McKinsey emphasize the need for scale, but neither fully accounts for the "Integration Tax." In the AI era, M&A failure usually happens at the data layer. If you acquire an AI-native company but cannot integrate its vector database or reasoning history into your core platform, you haven't bought a capability, you've bought a silo.

Organizational Readiness: McKinsey highlights organizational change, but the reality is sharper. You cannot run an Outcome 2 company with an Outcome 1 org structure. AI-native systems require different product management instincts (probabilistic vs. deterministic) and higher risk tolerance. M&A often fails here because acquirers force "SaaS-era" metrics on "AI-era" acquisitions, crushing the very velocity they tried to buy.

The Three Games of M&A

The "Inorganic Edge" in 2026 isn’t just about doing deals; it’s about knowing which game you are playing. The data suggests that M&A serves a fundamentally different purpose in each outcome:

In Outcome 1 (Surface Area), M&A buys you “relevance”. You are acquiring features to keep your product in the conversation, buying time while you figure out your long-term play.

In Outcome 2 (System), M&A buys you “architecture”. This is where the alpha is. You are not buying revenue; you are acquiring the reasoning engines and data layers that allow you to collapse silos and own the decision loop.

In Outcome 3 (Infrastructure), M&A buys you “control”. For hyperscalers, deals are defensive moats designed to secure the vertical supply chain and protect margins against inevitable commoditization.

For most SaaS executives reading this, the danger is getting trapped in Outcome 1 while pretending to be in Outcome 2. You cannot feature-stuff your way to a system-level valuation. The only way out is to use M&A to fundamentally re-architect the business, before the market permanently reprices you as "Legacy."

If you’re building, buying, or operating in this space, I’d love to compare notes. You can reach me at faraaz@inorganicedge.com or on LinkedIn.

Sources

Battery Ventures State of AI 2025 Report

https://www.battery.com/blog/state-of-ai-2025/The state of AI in 2025: Agents, innovation, and transformation

https://www.mckinsey.com/capabilities/quantumblack/our-insights/the-state-of-ai